Problem-based Approach to Accounting Education: Pragmatic Appraisal of a Technologically Enabled Solution

Carla L. Wilkin and Phillip A. Collier

Monash University, Australia

Good teaching is a journey rather than a destination. Inertia is an insidiously powerful negative force in teaching—the urge to keep doing things the way we’ve done them. Flachmann (1994, p.1)

ABSTRACT

Following calls for change to enhance accounting education, we describe and justify a ‘new pedagogy’ that centres on realistic business problems in the context of a simulated business and its authentic enterprise system. The aim is to prepare accounting students for a broader role in business decision making by providing them with relevant robust usable knowledge. Using design science methodology we describe three approaches to create artefacts that involve use of an enterprise system which support this proposal. Our contribution is an appraisal of these approaches. Included are examples of applying the pedagogy that demonstrates its feasibility.

Keywords: Technology; enterprise systems; processes; pedagogy; design science methodology.

INTRODUCTION

A fundamental tenet of the accounting profession is that accounting information is important for business decision making (McCarthy et al., 1982). In virtually all large companies accounting information is recorded, managed and often analysed in enterprise systems. Consequently we have witnessed an increase in the importance (and complexity) of enterprise systems and broadening in scope of the financial and non-financial information they provide. This shift evidences that ‘many of the traditional, essential skills of CPAs [professional accountants] are being replaced by new technologies that are increasing in number and being rapidly developed’ (AICPA, 1998: 3). Accordingly as accountants increasingly use these systems to support business decision making, they must be educated in the operation of technologically enabled business processes, including at the tertiary level.

Enterprise systems provide support for managing business processes. Accountants need to understand these processes so they can understand the risks that are present and highlight the internal control problems. This creates a significant opportunity for the accounting profession to take a central role in the configuration and management of processes within an enterprise system (Arnold & Sutton 2007). As a result it is no longer enough for graduates from the accounting profession to be narrow technical experts in financial or management accounting. Instead they must be able to relate their knowledge effectively to the broader business environment (Dunn & McCarthy, 1997).

This highlights the need for accounting education to respond to the influential calls for change so students are better prepared for the accounting profession of the future (e.g. Albrecht & Sack, 2000; Mathews et al., 1990). In particular the accounting curriculum must evolve to embrace this changing context within a wider remit of theory and concept development (AICPA, 1998) – a view that has long been endorsed by the accounting bodies (Bromson et al., 1994). In response, our work builds on and extends prior work by providing a comprehensive proposal for incorporating enterprise systems into an accounting curriculum. Our proposal includes a detailed design for a problem-based approach to learning in accounting education, which is authentic by being situated in a simulated business.

This paper first provides a more detailed background about the call to action from the profession, academics and regulators, together with an overview of prior literature on transforming accounting education. We then present our response, where we describe and justify a ‘new pedagogy’ and the importance of processes to an accounting curriculum. The main contribution of this paper is the presentation of options for a new model that provides authentic learning activities for students and an overview of how necessary resources can be created, including configuration of an enterprise system for student use. Included in this discussion is an instantiation of a new design to demonstrate its feasibility. Our conclusion includes discussion of future opportunities and challenges.

BACKGROUND AND CALL TO ACTION

A large-scale project Accounting Education: Charting the Course through a Perilous Future1 (Albrecht & Sack 2000) investigated a decline in the number of students choosing to major in accounting. Through a survey of accounting graduates, the authors found that students would choose a different major if given a second chance. One stark conclusion from this study was that ‘Corporate and public accounting firms are working hard to transform themselves into finance and professional service firms. It is now accounting education’s turn to transform itself’. Whilst the number of students studying accounting has grown, a shortfall of qualified accountants exists, as evidenced by accountants being listed on the Migration Occupations in Demand List (www.dimia.gov.au). Further, China has signalled a desperate need for accountants (Coonan, 2007). This creates an exciting opportunity for accounting educators to evaluate their curriculum.

Traditional accounting systems embody a limited ontology that focuses primarily on financial transactions, which significantly limits their applicability to a technology enabled wider business perspective (Walker & Denna 1997). The resource-event-agents (REA) extended accounting model overcomes this limitation by providing an integrated theory of accounting and non-accounting information (McCarthy, 1982; Geerts & McCarthy, 2002). Strong conceptual links between REA diagrams and enterprise systems highlight the importance of this development. For example, the widespread use of enterprise systems has ‘… radically change[d] the way accounting and business information exists within organizations, …’ (Sutton, 2000: 6). In practice the role of accountants is rapidly changing to that of strategic business partners who help ‘national and international organizations to meet their challenges’ (KPMG, 2006) by leveraging potential from IT use (Sutton, 2000). So what does this mean for accounting education?

Arnold and Sutton (2007) suggest that accounting students should achieve ‘an understanding of core business processes in both retail and manufacturing enterprises’. Enterprise systems are capable of modelling cross-functional business processes and tracking their execution. Consequently accountants need to be less concerned with individual transactions (Sutton, 2000), and more concerned with understanding business processes and how these function in a technology enabled environment. Importantly, if processes are configured correctly, then each component transaction will be executed correctly, assuming no deliberate interference with the system or its data. For business this means more readily available data and analytical tools to inform timely decision making. For auditors this means less emphasis is placed on individual transactions with a ‘… move towards assessing a company’s business processes and practices, and… a move towards increased emphasis on internal controls over the reliability of information systems’ (Sutton, 2000: 4).

Provisions concerning the definition and management of business processes contained in the US Sarbanes-Oxley Act (2002) require firms to establish a financial accounting framework to produce financial reports that are readily verifiable and traceable to source data. This can be achieved by modelling processes; assessing processes for their quality; and attesting to processes executing effectively. Such provides a foundation for what Davenport (2005) calls ‘The coming commoditization of processes’. He posits that processes need to be defined and documented to enable effective outsourcing of non-core business operations, commonly referred to as business process outsourcing (BPO). These requirements create a significant opportunity for the accounting profession to take a central role in the configuration and management of processes within an enterprise system.

In practical terms accounting graduates will often be responsible for technologically enabled business processes, whether as users, designers and/or owners (Gelinas et al., 2004). A process user would know how the process is controlled, what information is captured and stored, and how such information can be used to manage the business more effectively. A process designer would have knowledge about what, when, and how events are recorded, and the range of controls available in a system. Finally, a process owner may be required to stipulate controls and assess the processes’ efficiency and effectiveness. All three perspectives can be targeted by the pedagogy described in this paper. Whilst the roles of designers and owners are perhaps the most relevant to tertiary accounting education, the user perspective is arguably a necessary pre-requisite.

In summary, professional accounting is no longer dominated by dispassionate rules; there are choices and trade-offs in assessing and configuring technologically enabled business processes and their controls. For example, as accountants become pivotal in ‘Monitoring and Evaluating Performance’ (Nah et al., 2001), we need to expose accounting students to business operations and enterprise systems, and educate them in the context of this rich backdrop. This will help to shift graduates from being experts in financial or management accounting; to developing their knowledge about the broader business environment and the role technology plays.

We propose a curriculum that develops the knowledge, skills and technological skills required of accounting graduates, including their ability to:

- assess rules and processes embedded in an enterprise system for conformance/validity with that required/desired;

- assess the adequacy of changes to the configuration of an enterprise system;

- execute changes to the configuration of an enterprise system appropriately;

- examine enterprise system processes for robustness;

- evaluate the reliability of the system; and

- generate reports to support analysis of financial and operating performance (Arnold & Sutton, 2007).

Significant barriers need to be considered. Enterprise systems are highly complex, and require high-capacity server hardware. Further, knowledge concerning how to use them effectively is scarce, especially amongst academics (Becerra-Fernandez et al., 2000; David et al., 2003). Whilst the knowledge barrier still remains2, enterprise system vendors, such as SAP and Oracle, have been proactive in providing software licences and support through academic alliance programs. Further, SAP’s provision of remote access to the software using the Web has diminished technical difficulties and costs.

Students have also been cautious given it has been found that they ‘do not see how a particular hands-on exercise relates to what they are learning about operations, or accounting, or information systems, in their coursework’ (Fedorowicz et al., 2004). To facilitate this and delineate between the training provided by enterprise system vendors, we need to focus our objectives on providing conceptual education (Davis & Comeau, 2004).

The literature is largely silent on how to respond to the calls for change to accounting education. For example, Albrecht and Sack (2000) are careful not to offer numbered recommendations and call for accounting educators to assess their environment and degree offerings and then create an appropriate strategic plan. We propose that one element of this strategic plan should be a ‘new pedagogy’ for accounting education. This ‘new pedagogy’ is required to address the broader, technological focus of the profession, a topic that is addressed in more detail below.

PEDAGOGY3

With the development of double-entry bookkeeping about 500 years ago, accounting systems have been able to systematically record all financial transactions. However, as businesses became larger through the industrial and technological revolutions, the systematic nature of accounting has become defined through principles, rules and standards. Public accounting attests to the importance of the systematic nature of accounting systems: the reliability of the system can in principle be verified. Of course for most of this period accounting systems were manual systems that accountants personally supervised and executed.

Not surprisingly then in tertiary accounting education, many of the accounting principles, rules and standards have commonly been delivered via lectures, with application of the rules and standards addressed in tutorials. Arguably transmission and practice were very appropriate for this type of knowledge, especially when used later in manual accounting systems. However, this is no longer the case. Enterprise systems have taken over the routine aspects of recording journal entries, organizing entries into ledgers, and generating reports.

With automation of accounting rules and standards, and a shift in focus of the profession towards dealing with less structured problems and trade-offs, the transmission pedagogy is deficient. Although knowledge of accounting principles, rules, standards, and processes is important, the ability to analyse trade-offs and choices with respect to business needs is not readily transmitted. Consequently, we propose a shift to a more cooperative process of teaching that focuses on student-centred learning and encouragement of problem-solving skills (Ramsden, 2003). This approach is based upon the convergence of many educational theories from the constructivist perspective (Jonassen & Land, 2000).

Such a move involves providing an authentic context for students to find meaning for newly introduced accounting concepts, as espoused by the philosophy of situated cognition (Brown et al,. 1989). This approach is based on the theory that knowledge is best developed in the context of activities where it will be commonly used. For accounting education this implies that students recommend trade-offs and choices for a simulated business and its authentic enterprise system, with the aim to use their existing knowledge while constructing new knowledge of accounting concepts and technologically enabled business processes. Such experiential learning (Kolb, 1984), linked with authentic problem-solving, fosters the construction of deep holistic knowledge (Ramsden, 1992; Bromson et al., 1994; Milne & McConnell, 2001). In particular, this pedagogy discourages students from focusing solely on memorizing and encourages critical thinking.

Deep knowledge is useable robust knowledge (Brown et al., 1989) that has a positive association with three important and desirable educational outcomes: a more positive attitude; richer understanding; and higher marks from students (Ramsden, 2003). For accounting professionals, the acquisition of this form of knowledge is essential given that the business problems they face are often ill-structured. Further, given the association with a more positive attitude and higher examination marks, it should lead to higher levels of student engagement and, in turn, help to overcome the negative attitude of accounting graduates reported by Albrecht and Sack (2000).

Provision of an authentic context for accounting education now necessarily includes practical experience with an enterprise system. Situated learning activities can then require students to use the system to find and perhaps provide information and process knowledge relevant to analysing and solving a business problem. The focus of these problems is conceptual development, but in the process, students should gain skills in using and configuring enterprise systems. Beyond basic familiarisation with the enterprise system, which could be partially self-directed, students should be able to acquire these skills as they need them, in common with the principles of a problem-based approach to learning.

LEARNING ABOUT PROCESSES

Experience in integrating enterprise systems into university-level curricula has grown, particularly with the aid of SAP’s educational alliance program (see, for example, case studies in Watson & Schneider, 1999; Hawking & McCarthy, 2000; Rosemann & Watson, 2002; Fedorowicz et al., 2004). From a practical perspective, recent impetus for the use of these systems in the curricula concerns their ability to integrate the functional silos within a business curriculum (for example, Davis & Comeau, 2004; Johnson et al., 2004). However, there is more work to do. For example, in the accounting domain, pioneering literature has focused on providing student experience with enterprise systems without attention to pedagogy (David et al., 2003; Jones & Lancaster, 2001).

Our contribution to enhancing accounting students’ learning about processes is structured using design science methodology. This methodology is used to understand, explain and improve the real world by creating innovative artefacts in a well-defined manner that address specific problems (vom Brocke and Buddendick, 2006, p.581). Using March and Smith’s (1995) framework for design science, we present a problem-based approach to learning that involved creating a new conceptual design (Hevner et al., 2004) from both managerial (in this case accounting education) and technical perspectives. This approach demonstrates how authentic learning activities can be created to support learning about processes from an accounting perspective and provides examples that demonstrates its feasibility.

In our approach we provided students with an authentic context, namely a technologically enabled business enterprise, through which they were encouraged to actively engage with the real world of accounting. In our case studies we systematically explored (Brown, 1999; Cavana et al., 2001) rich student experience with the artefact and thus the implications for student learning. The three instantiations used variations in conceptual design such that we could appreciate whether the variations in approach impacted student learning.

In reporting on our endeavours we focus principally on the first case study because it was our initial attempt at this technological approach to learning. Later iterations (Case Studies 2 and 3) drew directly upon this initial exercise. The primary case study employed a new method that entailed configuring an enterprise system with an authentic replica of business information and processes for student use. In reflecting on our experiences, we used several methods to gather data about students’ experiences. In Case Study 1 students completed a short quiz that gave them an opportunity to express their views on the best and worst features of the unit. This and their evaluation of teaching performance provided data about the merits of the changed curriculum. For Case Study 2, a change in teaching staff meant we only had access to unstructured feedback. In Case Study 3, student evaluations of teaching performance and a survey of the students provided quite comprehensive understanding of their views about the merits of the new approach. We conclude our pragmatic appraisal by reporting on some outcomes from this learning approach and related consideration of student engagement with technologically enabled business processes.

Conceptual design

Business processes are sensitive to the passage of time. That is, the partial order of business events determine the stages of a process, where each stage determines a current status of the process. Process designers need to consider variations on the normal sequence of events to ensure appropriate detection and/or control of exception or undesirable situations. Enterprise systems are configurable to manage the set up and execution of processes according to a wide range of potential process designs.

As students engage with and learn about business processes and their embedded controls in a realistic setting, it is important to be able to isolate a stage and characterise the status of the process at that point in time. Thus, a sequence of stages provides a step-by-step walkthrough of the process, where each subsequent stage is the result of one or more business events having occurred. Further, in a learning environment it is desirable to be able to halt a process so that the current status can be investigated and alternative courses of action or process design explored.

Our desire to be able to freeze time so students can investigate and experiment with processes, and when necessary recover from mistakes, means it was not feasible to provide students with access to an operating business and its installed enterprise system. Instead we required a simulation4 of a business and its infrastructure, which included access to an authentic enterprise system. Furthermore, the business needed to be depicted in a manner that was consistent with the way in which the enterprise system had been configured and with sufficient detail to provide access to resources required for learning activities. Web technologies helped achieve this aim. Herein an intranet portal was interfaced with the enterprise system that had been customised for key business roles, and the company intranet that had been simulated to provide access to key resources.

Configuring learning activities

To create authentic and situated learning activities, a learning objective was first required e.g. ‘investigate internal controls relevant to applying cash, focusing on the trade off between protecting an enterprise from bad debts vs. satisfying legitimate customer needs’. The learning objective was then used to create one or more relevant back stories within the simulated business. The back story was described in terms of one or more roles, plus any relevant history and prior interactions with the process. Concurrently, business information consistent with the back story was provided in the enterprise system. Typically the story unfolded as a sequence of business events, and the student had access to a staged scenario of symptoms consistent with the back story. Importantly the information released did not include all relevant details. Students were tasked to undertake investigations, including the use of the enterprise system, and make recommendations about how to handle issues that arise within the scenario.

Connected to this was a decision about whether students were invited to simply access information from within the enterprise system, or whether they were also required to provide information. In our initial exercise we chose to provide students with read-write access. In contrast, our second case study reports on students’ engagement when using the system in read-only mode. Our initial exercise involved read-write access as we believed it was beneficial for students to gain experience with identifying and entering ‘correct’ information into an enterprise system. At a more advanced stage, learning activities may involve rectifying data entry errors, and/or configuration of the enterprise system. Learning activities that involve data entry involve much more complexity in management of the enterprise system, especially for large classes, but in Case Studies 1 and 3 we provide a design for how this can be achieved.

Because no two businesses are identical, enterprise systems are designed to be highly configurable5. They typically consist of core modules to manage the general ledger and company contacts, plus optional modules capable of managing other business functions. As such they frequently cut across traditional boundaries between business units. Consequently, these systems are daunting to envisage in an educational context, certainly by individual academics. Instead a concerted team effort is required to make them accessible to students (Rosemann & Watson, 2002).

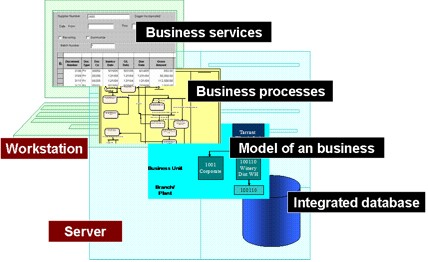

A typical deployment of an enterprise system can be configured to provide different business roles with access to relevant business services6 through desktop workstations. The business services, in turn, provide one or more views on a range of different business processes that are configured for specific branches, functions and locations of the focal business operations (see Figure 1). Unless there is a major technical problem, business information is continuously aggregated over time and will usually not revert to a previous state.

Figure 1: System architecture of an enterprise system.

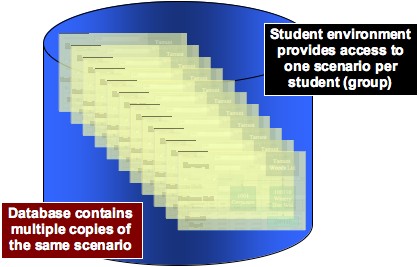

On the one hand, if students are solely granted read-only access to information contained within the enterprise system, configuration is just like a business installation with one copy of the information relevant to the current stage of a scenario. Under this approach, security settings need to be configured in such a manner that no information can be added or changed by students. On the other hand, if students are permitted or required to enter information (i.e. read-write), a separate copy of the current stage of a scenario is required for each student or student group. This can be achieved by adding multiple copies of the scenario to the database using different companies and associated entities. In this case security needs to be set so that user IDs can only see one instance of the companies and associated entities. A scripting language, or similar, will be required to create multiple copies of the business information for each student. Figure 2 depicts the result of this set up.

Figure 2: Separate copies of the configured business services managed in one database to cater for read-write access.

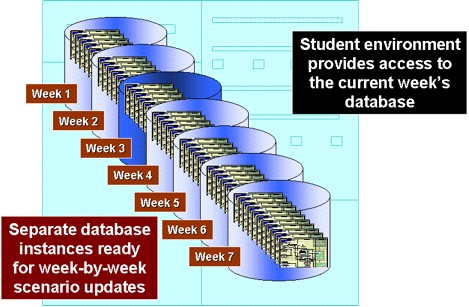

Enterprise systems track progress through the stages of a process using configurable status codes, where a business event may (conditionally) update the status code and thereby move the process onto the next stage. If students have read-write access to an enterprise system they can initiate an event themselves and observe its effect. The risk here is that some students will make errors and/or explore further than necessary for one week’s exercise. A solution to this is to have a second database available that can demonstrate a sample outcome from a new business event. In general, this approach enables students to explore a scenario and its consequences one week, then reflect on their experiences, and in the following week examine a sample outcome from completion of the previous week’s activities. If students have read-write access to the subsequent week’s database, then it is necessary to pre-prepare multiple instances of this version of the business information (see Figure 3).

Figure 3: Server at Week 1 showingweekly progression through authentic scenarios.

Using an enterprise system in this way means that the business information for the staged releases needs to be created well in advance. Whilst we’re yet to determine the minimum latency possible, a commitment to learning activities and necessary business information is required several months before students undertake the learning activities.

THREE CASE STUDIES APPLYING THIS UNDERSTANDING WITHIN THE CONTEXT OF BUSINESS PROCESSES.

Scenario for Case Studies 1 and 2: ABC Wines

To demonstrate the feasibility of the model described above, we created an authentic winery business, ABC Wines. Our department had an educational licence to run the JDEdwards EnterpriseOne (now part of the Oracle family) enterprise system. A winery business7 was seen to be a good choice for several reasons:

- a winery can include aspects of primary production, manufacturing and retailing, thus providing a broad scope of potential issues;

- wine making is part of an important and successful industry;

- at the time of settling on the business case study, the JDEdwards company was building a winery module for their EnterpriseOne system, something we could potentially use at a later date; and

- a local winery that uses JDEdwards EnterpriseOne offered us assistance in configuring EnterpriseOne to model their own configuration.

Whilst we were concerned about various national and cultural sensitivities among our students with respect to alcohol, the executive of the department where this subject was offered deemed these to be outweighed by the advantages outlined above.

According to our case materials8:

‘ABC Wines commenced operations in March 1998 (we wanted historical data) when ABC Pty Limited acquired ownership of a 10-hectare vineyard in Smithfield. Since its incorporation, ABC Wines has grown from a small start up vineyard to become a medium-sized winery in the world market with four different wine labels. This growth has been achieved through two streams. Specifically, within ABC Pty Limited a vineyard, cellar door outlet, tourism services and the blending and bottling of ABC Wines have all contributed to revenue growth. Additionally the acquisition of three separate wineries between 2000 and 2004 has seen the annual turnover of the group grow to $45 million dollars.’

Behind the scenes ABC successfully used QuickBooks Pro as its accounting information system in its early years. However, as a result of acquiring other wineries, business processes became disjointed, inconsistent across different business units and inefficient. Moreover, management wasn’t able to extract the data and reports needed to monitor strategy and they believed there was a lack of internal control. ABC therefore acquired a new business information system, JDEdwards EnterpriseOne, initially to support their own operations, with a longer-term plan to expand the system to cater for the operations of the newly acquired wineries.

Based on this scenario and with help from the local winery, JDEdwards EnterpriseOne was configured as the business information system for ABC. For the purpose of the learning activities that involved use of the enterprise system, a limited range and quantity of business information was created. This mainly focussed on ABC’s sales and procurement processes. Using this case study, authentic learning scenarios that described parts of ABC’s operations, which included the use of their business information system, were constructed.

This was the basis for producing learning activities for many hundreds of first year tertiary students. The learning activities were included in a first year subject, Accounting 3. In the first implementation which took place in 2005 (Case Study 1), students had read-and-write access to the system, whilst in the second implementation in 2006 (Case Study 2) students were restricted to read-only access.

Case Study 1: Read-write access

In Semester One 2005 Case Study 1, which permitted full read-write access to the enterprise system, was implemented. The project was enthusiastically championed by one of the co-authors and followed the full generality of our model shown in Figure 3 above.

As shown in Figure 3, our major technical innovation concerned the use of replicated copies of the business information in different companies and associated entities in an enterprise system. Tight security settings were used to ensure that each student ID could only access functionality relevant to their current role and the current scenario. Further, security settings restricted access to information concerning the entities allocated to each student ID. The added burden of setting up this security infrastructure could be avoided if students could be trusted to only write to their own entities.

Case Study 2: Read-only access

In Case Study 2 a new academic took over administering the subject and opted to utilise the alternative configuration of the enterprise system, namely to allow students read-only access to the scenarios. This option required configuring the enterprise system with a single copy of an authentic business. Such an approach certainly made for easier management of tutorials and associated discussion, but created a potential risk that students would see their engagement with the system as less interactive and therefore possibly less relevant to “real world business scenarios”. This approach was trialled with the ABC Winery Scenario in 2006 with the same first year accounting subject, using the same technical support, the same group of tutors, but a different lecturer.

Case Study 3: Read-write access

By 2006, one of the champions behind this problem-based approach to accounting education had moved to another university. Being convinced of the value of this problem-solving approach to understanding business processes using technology, she began again the process of implementing this curricula initiative, albeit with a tight budget but with Faculty support. Drawing on past success, a read-write approach was adopted, but this time the technical infrastructure, server configurations and technical support were outsourced by using an educational alliance program established by JDEdwards’s chief competitor SAP. This provided the educational licence to use SAP. Building on past experience, the academic involved created new relevant scenarios to engage student interest and related course materials. Moreover, unlike Case Studies 1 and 2, this subject was taught at post-graduate level in 2007 and 2008.

One significant outcome of Case Study 3 has been that, based upon Faculty recognition of the value of the learning outcomes, the subject has become a core (compulsory) unit in the Master of Business (Accounting) degree.

A PRAGMATIC APPRAISAL OF THE ALTERNATIVES

Evaluation of the alternative designs

Read-write access: A reflection on Case Studies 1 and 3

As described above, pedagogically such an approach involved providing an authentic context for students to find meaning for newly introduced business concepts, as espoused by the philosophy of situated cognition (Brown et al., 1989; Kolb, 1984). This is based on the theory that knowledge is best developed in the context of activities where it will be commonly used. For accounting education this implies that students recommend trade-offs and choices for a simulated business and its authentic enterprise system, with the aim to use their existing knowledge while constructing new knowledge of accounting concepts.

Did this approach, in line with Ramsden (2003), achieve a more positive attitude; richer understanding; and higher marks from students? Using the University’s quality of teaching instrument, indications from student ratings of lectures and tutors imply these were achieved. In terms of teaching ratings, we achieved a 20% increase in students’ satisfaction with the unit. Tutors anecdotally reported more informed comments in tutorials that implied a richer understanding. Additionally, examination results improved compared with previous semesters.

In Case Study 1, more formative feedback (whilst somewhat brief in nature) on use of the system was acquired from a short quiz conducted in tutorials where students were asked to comment in writing on the best and worst aspects of the unit. We report in Table 1 those that directly relate to the learning activities that involved use of the enterprise system.

Table 1: Quotations from students about the best and worst features of the unit

Panel A: Best Features |

“Real feel for the JD Edwards program” |

“Give me a great knowledge on computing process and ERP system” |

“Good intro to ERP system” |

“Computer based exercises in the tutorials” |

“More knowledge about how does a business operate” |

“Give more understanding about business cycle” |

“Seems very useful and perhaps can help me in the real economic world after graduate” |

The unit “is good introduction to how business processes work as it is useful for later once students enter the job” |

“To understand in more detail about how the systems work” |

“The benefit of using the ERP system was a good learning experience” |

“The introduction to the ERP is excellent as I don’t think many universities offer this opportunity” |

Panel B: Worst Features |

“Need a bit more interactivity with system (but that maybe because I have a more technical background)” |

“Hard to understand, not only the word, but also the idea or perhaps I’m not the person good at IT” |

“Have no idea why we have to study the software (JD Edwards)” |

“Incorporating JD Edwards into tutorial is not of much help to my understanding. I rather tutorial time is spend more on “practice” for interpreting/understanding the flowchart” |

What is clear from this table is that some students did appreciate the authentic nature of the learning activities. Interestingly, the background of students appeared to determine their reaction to such a complex information system e.g. one wanted to be able to roam more freely, whilst another was less confident with IT. Further, informal feedback from students indicated they took a bit longer than normal to prepare for a tutorial, but not much.

In Case Study 3, the outcome was equally well worthwhile. The overall teaching rating was 4.53 (on a 5 point scale), which placed it in the top 5% of units taught within the Faculty of Business at one of Australia’s largest universities. In fact, identical ratings were achieved in this unit in subsequent offerings. Further, a survey conducted with students specifically revealed that the students appreciated the technological approach (see Table 2).

Table 2: Student perceptions of subject value

Statement |

Score (Maximum is 5 which means strongly agree) |

Found the first hand knowledge of SAP in this unit valuable. |

Mean: 4.81. |

Found the practical handouts guiding them through the SAP system helpful. |

Mean: 4.50. |

Said the use of SAP had helped their understanding of accounting and related concepts. |

Mean: 4.35. |

Thought the unit enabled them to feel better prepared for the workforce. |

Mean: 4.62. |

Would recommend this unit to fellow students. |

Mean: 4.73. |

Said this unit was one of the most valuable that they have studied at the university. |

Mean: 4.35. |

Illustrative student comments include:

- “I could experience…. using sophisticated software such as: SAP ERP…very priceless experience”.

- “This unit is truly one of the best units that I have studied at the university. It will certainly open doors for my future job interviews. And SAP is the buzz word in business around the world”.

Read only access: Reflection on Case Study 2

The read-only method was used once in 2006 and not repeated. Student attitudes were less positive and feedback clearly indicated that the distinctive value of the approach, namely to foster problem-solving as a learning strategy, was lost in translation from the read-write approach to the read-only approach. Without the obvious positives, the heavy demands of this approach on budget, teaching personnel and time, made it easy to justify a return to the old pedagogical approaches.

Whilst these results do provide some insight, as tutors and lecturers become more comfortable with the curriculum there’s a need to conduct more rigorous evaluation to gauge student reaction in more detail about their perception of learning outcomes. Nonetheless the approach using read-write access appears to be heading in the right direction.

REFLECTION ON THE OUTCOMES

Albrecht and Sack (2000: 3) issued a blunt a challenge that ‘we cannot save accounting education by continuing to do more of the same’. In response, the authors have contributed the design of a new model for a problem-based approach to learning that situates students in an authentic context, namely a technologically enabled business enterprise. This pedagogy is based on prior literature, which empirically demonstrates some of the virtues of this approach. Furthermore, these same virtues meet several of the challenges set by Albrecht and Sack (2000). The design has been instantiated and use by students demonstrates its feasibility. Such application shows the potential to extend problem-based learning from the currently predominant use in small group teaching to larger situations, even with more complex settings.

We conclude that as with any significant change to an organization, success will be more readily achieved with a powerful champion to a cause. In a sense a technological innovation like ours is a strategic initiative and strategy will only be successful if it is incorporated into organizational goals. The success of the technological innovation did require leadership, coordination and commitment as well as the capacity to understand the effect of the required changes upon the student and teaching cohort including impacts on university budgets and facilities (Beath, 1991; Clemons, 1998; McKersie and Walton, 1991; Wilcocks and Sykes, 2000).

There is no doubt that adopting our interactive design from scratch is an large task, particularly given that it requires the creation of a new authentic business and configuration of an enterprise system to be consistent with this business description. Basing this on a real business or building on authentic business descriptions are ways to reduce this burden (see also, Johnson et al., 2004). Equally using outsourced technical infrastructure and services facilitates implementation. With the ability to deliver learning activities using Web technology, this task could be tackled by a consortium or publisher who would be able to take advantage of large scale delivery to recover the relatively large fixed cost. Furthermore, when the enterprise system infrastructure required to run such a proposal is provided through educational alliance programs a significant technical risk is eliminated.

Our design has deliberately remained silent on the topic of accounting curriculum. Given the comprehensive and integrative nature of large enterprise systems like Oracle and SAP, it would appear to be suitable across a wide range of accounting topics, assuming a desire to adopt a problem-based approach to learning. There is undoubtedly a significant role for scaffolding support as students need to learn about the dispassionate accounting rules and standards, and for efficiency reasons alone, this may still be best approached using transmission through lectures. There may also be room for a case-based approach to address issues that cannot be realistically treated in the fully developed authentic business(es).

Unlike David et al. (2003) we have shown that resources or costs can be worked through.

However, a clear tension exists between student read-only access to the enterprise system and full

read-write access. We believe that the learning experience would be significantly compromised,

and would become unrealistic, if all data entry to an enterprise system were to be disabled.

However, it is possible that providing read-only access delivers a substantial proportion of the

learning benefits at a fraction of the cost. Too much data entry could also engage students in a

perceived training exercise, which is a clearly defined role that is typically reserved for system vendors.

Therefore, while providing practical skills, balance needs to be maintained to achieve creation of deep

knowledge about accounting concepts, which is an important outcome at a University level.

The emerging opportunity that may help to overcome the resource-intensive nature of our design is the

integrative nature of enterprise systems. Several authors have used this as a motivation to incorporate

enterprise systems into a business curriculum, sometimes as a capstone (for example, Davis & Comeau, 2004; Johnson et al., 2004). This concept offers much promise for moving forward with accounting education.

CONCLUSION

The range of case studies described in this paper (wherein we investigated the place of problem-based learning in accounting education) shows that the concepts can be successfully applied in units with both small and large student numbers. Certainly it is evident that success is reliant upon strong commitment from the chief stakeholder (unit coordinator) together with strong departmental support. This support needs to be more than simply a financial commitment: resource allocation, administrative support and ownership of the value of the undertaking are all equally important for successful outcomes.

However, enterprise systems by their nature are infrastructure and arguably should intrinsically form part of the technological infrastructure of business education.

In this role they should be introduced in the first year of a business curriculum, with all students in attendance; so it becomes ‘core’ to a business degree. If this were the case, there may be a scramble by departments to claim ownership of the subject and thereby access to the substantial resources that would flow. In our case studies, we have demonstrated the application of a ‘new pedagogy’ that centres on realistic business problems in the context of a simulated business and its authentic enterprise system. The pedagogy, with its aim to prepare accounting students for a broader role in business decision making by providing them with relevant robust usable knowledge, is consistent with our educational vision for enterprise systems in University education: we leave the politics to others!

Endnotes

1 Albrecht and Sack (2000) is based upon a large-scale project supported by the major accounting professional bodies and employers in the USA. The report expressed the views of individual professionals and high-level academics, and synthesized empirical evidence.

2Even the visiting academic initiative proposed by Hawking et al. (2004) for the SAP educational alliance is challenged by the continual change in the capabilities of enterprise systems.

3In this paper we define pedagogy to mean the ‘activities that facilitate knowledge construction’.

4For the purposes of this paper we use simulation to refer to a relatively passive model of a real business that can be probed and possibly changed. Students experience first hand controls and routine responses from the enterprise system. Substantive responses from the simulated business and its supply chain are designed and ‘released’ manually.

5 We distinguish between configuring a business information system, where 'details of the system are mapped and fitted to the details of the process, and vice versa' (Davenport 2000, p. 150). This is distinct from customization, where fundamental changes or additions to a business information system are necessary, usually involving writing some program code, to suit the needs of a business.

6 We tend to characterise enterprise systems as providing a set of business services, rather than as a complex IT-based resource. This aligns with the perspective of a business analyst who is tasked with system configuration to provide services to record, monitor, analyse, and report on the state of business operations. This contrasts with the role of a system engineer who is concerned with the installation and maintenance of an IT-based resource to provide such services in a secure and reliable fashion.

7 JDEdwards EnterpriseOne was delivered with a pristine environment, aka ‘Demo Junior’, which contains some business information relevant to a bicycle wholesaler. However, (1) documentation about the bicycle wholesaler’s business strategy and situation apparently does not exist; and (2) the business information is simultaneously too complex in some aspects and too incomplete in others. As such, we judged the pristine environment to be an inappropriate basis for the authentic business required in this project and hence we created ABC.

8 A full version of the case study is available from the authors.

APPENDIX A: EXAMPLE OF A LEARNING ACTIVITY

The learning activities constructed using ABC and its enterprise system required students to use EnterpriseOne to investigate the current status and recommend possible solutions to problems. For this learning activity, the learning objective is to ‘investigate internal controls relevant to applying cash, focusing on the trade off between protecting an enterprise from bad debts vs. satisfying legitimate customer needs’. This required students to have read-only access to the ABC enterprise system for Stages 1 and 2, plus write access for Stage 3. The scenario involved one stage in an automated process, but spins off a manual sub-process.

Scenario—Stage 1

A customer calls ABC irate that the order they’ve placed a week ago has not been fulfilled. The customer threatens to cancel their account with the company. The Sales Manager is unaware of the problem and queries the sales order in the system. When students retrieve the customer’s order in the system and investigate this problem, they find that the status of the order is ‘on credit hold – aging’, which explains the immediate cause of the problem. Students are asked: what has caused this status to be assigned; why a customer may be placed on credit hold; why they think the customer wasn’t notified that they were on credit hold; what they think the Sales Manager should do to resolve the situation; and how the process could be improved to avoid the situation from recurring.

Scenario—Stage 2

Following a relatively shallow analysis, the Sales Manager explains to the customer that their order is on credit hold because of unpaid invoices. The customer claims that invoices have been paid according to the normal terms of trade and can quote the cheque number to back it up. Students are requested to investigate this claim and explain why it has happened, and what can be done to fix it.

Scenario—Stage 3

The Sales Manager can’t change the credit limit and they can’t get hold of the Credit Manager or anyone with authority to fix the problem. Thus, they resort to using a 3-part manual sales order and picking ticket to re-initiate the order. Students are presented with a copy of the physical documents, and asked to comment on whether they thought sending the goods using a manual sales order was appropriate to the circumstances; why the Sales Manager can’t change the credit limit; suggestions of who would be able to change the credit limit; and why prices are blanked out on the Picking Ticket, but not on the Sales Order.

Scenario—Stage 4

Students are asked to investigate the customer’s accounts receivable details in the system. This more sophisticated investigation of unapplied cash reveals that money received was not credited against the correct invoices and instead was credited to unapplied cash. In light of what they’ve found students are asked to brainstorm reasons why there might be unapplied cash; which invoice the unapplied cash should be applied to; and the consequences of having unapplied cash. Finally, after reviewing the order in the system the next day to check that the system reflects the correct status codes, the students are asked to reflect on what has happened. In particular they are asked to consider how the actions in one process can affect other processes achieving their goals.

REFERENCES

Albrecht, W. S. & Sack, R. J. 2000. Accounting education: Charting the course through a perilous future, American Accounting Association, Accounting Education Series, 16, [accessed 20 Sept 2004, available from http://aaahq.org/pubs/AESv16/toc.htm].

American Institute of Certified Public Accountants (AICPA), 1998. CPA vision project: Focus on the horizon [accessed 20 Sept 2004, available from http://www.cpavision.org/vision.htm].

Arnold, V. & Sutton, S. G. 2007. The impact of enterprise systems on business and audit practice and the implications for university accounting education, International Journal of Enterprise Information Systems, vol. 3, no. 1.

Beath, C. A. 1991. Supporting the Information Technology Champion, MIS Quarterly, vol. 15, no. 3, pp. 355-372.

Becerra-Fernandez, I., Murphy, K. E. & Simon, S. J. 2000. Integrating ERP in the business school curriculum, Communications of the ACM, vol. 43, no. 4, pp. 39-41.

Bromson, B., Kaidonis, M. A. & Poh, P. 1994. Accounting information systems and learning theory: An integrated approach to learning, Accounting Education, vol. 3, no. 2, pp. 101–114.

Brown, C.V. 1999. Horizontal mechanisms under differing IS organization contexts. MIS Quarterly, vol. 23, no. 3, pp. 421-454.

Brown, J. S., Collins, A. & Duguid, P. 1989. Situated cognition and the culture of learning. Educational Researcher, January-February, pp. 32-42.

Cavana, R.Y., Delahaye, B.L. and Sekaran, U. 2001. Applied business research: Qualitative and quantitative methods, Milton Qld: John Wiley & Sons Australia Ltd.

Clemons, C. 1998. “Successful Implementation of an Enterprise System: A Case Study, Proceedings of the Americas Conference on Information Systems, Baltimore, Maryland, pp. 109-110.

Coonan, C. 2007. Shortfall in China: Nowhere is there more opportunity for Accountants than in China, In the Black, August, pp. 31-35.

Davenport, T. H. 2005. The coming commoditization of process, Harvard Business Review, June, pp. 100–108.

David, J. S., Maccracken, H. & Reckers, P. M. J. 2003. Integrating technology and business process analysis into introductory accounting courses, Issues in Accounting Education, vol. 18, no. 4, pp. 417–425.

Davis, C. H. & Comeau, J. 2004. Enterprise integration in business education: Design and outcomes of a capstone ERP-based undergraduate e-business Management Course, Journal of Information Systems Education, vol. 15, no. 3, pp. 287-300.

Dunn, C. L. & McCarthy, W. E. 1997. The REA accounting model: Intellectual heritage and prospects for progress. Journal of Information Systems, vol. 11, pp. 31-51.

Fedorowicz, J., Gelinas, U. J. Jr. Usoff, C. & Hachey, G. 2004. Twelve tips for successfully integrating enterprise systems across the curriculum, Journal of Information Systems Education, vol. 15, no. 3, pp. 235-244.

Geerts, G. L. & McCarthy, W. E. 2002. An ontological analysis of the economic primitives of the extended-REA enterprise information architecture. International Journal of Accounting Information Systems, vol. 3, no. 1, pp. 1-16.

Gelinas, U. J., Sutton, S.G. & Fedorowicz, J. 2004. Business processes and information technology, Thomson South-Western, Australia.

Hawking, P. & McCarthy, B. 2000. Industry collaboration: A practical approach to ERP education, Proceedings of the Australasian Conference on Computing Education, Melbourne, Australia, pp. 129-133.

Hawking, P., McCarthy, B., & Stein, A., 2004. Second wave ERP education. Journal of Information Systems Education, vol. 15, no. 3, pp. 327-332.

Hevner, A. R., March, S. T. Park, J. & Ram, S. 2004. Design science in information systems research, MIS Quarterly, March, pp. 75-105.

Johnson, T., Lorents, A.C., Morgan, J. & Ozmun, J. 2004. A customized ERP/SAP model for business curriculum integration, Journal of Information Systems Education, vol. 15, no. 3, pp. 245-254.

Jonassen, D. & Land, S. M. 2000. Theoretical foundations of learning environments, Lawrence Erlbaum Associates. Mahwah, NJ.

Jones, R. A. & Lancaster, K. A. S. 2001. Process mapping and scripting in the accounting information systems (AIS) curriculum, Accounting Education, vol. 10, no. 3, pp. 263-278.

Kolb, D. A., 1984. Experiential learning: Experience as the source of learning and development, Prentice-Hall, Englewood Hills, NJ.

KPMG, 2006. What we do. http://www.kpmg.com/About/What/, accessed 7 December 2006.

March S. & Smith, G. 1995. Design and natural science research on information technology, Decision Support Systems, vol. 15, pp. 251-266

Mathews, R., Brown, P. & Jackson, M. 1990. Accounting in higher education: Report of the review of the accounting discipline in higher education, Volume 1, July 1990, Australian Government Publishing Service, Canberra.

McCarthy, W. E. 1982. The REA accounting model: A generalized framework for accounting systems in a shared data environment, Accounting Review, July, pp. 554-578.

McKersie, R.B & Walton, R. E. 1991. Organizational Change. in M. S. Scott Morton (ed.), The Corporation of the 1990s: Information Technology and Organizational Transformation, Oxford University Press, New York, pp. 244-277.

Milne, M. J., & McConnell, P. J. 2001. Problem-based learning: A pedagogy for using case material in accounting education, Accounting Education, vol. 10, no. 1, pp. 61-82.

Nah, F. F-H., Lau, J. L-S. and Kuang, J. 2001. Critical factors for successful implementation of enterprise systems, Business Process Management Journal, vol 7, no. 3, pp. 285–293.

Ramsden, P. 1992. Learning to teach in higher education, Routledge, London.

Ramsden, P. 2003. Learning to teach in higher education, 2nd Ed, RoutlegdeFalmer, London and New York.

Rosemann, M., & Watson, E. 2002. Special issue on the AMCIS 2001 workshops integrating enterprise systems in the university curriculum, Communication of the Association for Information Systems, vol. 8, pp. 200–218.

SAP, 2006. Education alliances: University program. http://www.sap.com/usa/company/citizenship/education/university.epx, accessed 13 December 2006.

Sutton, S. G., 2000. The changing face of accounting in an information technology dominated world, International Journal of Accounting Information Systems, vol. 1, pp. 1–8.

vom Brocke J., & Buddendick, C. 2006. Reusable conceptual models – requirements based on the design science research paradigm. In: Hevner AR (ed) Proceedings of the First International Conference on Design Science Research in Information Systems and Technology. 24-25 February 2006, Claremont, CA, pp. 576-604

Walker, K. B. and Denna, E. L. 1997. A new accounting system is emerging, Management Accounting, vol. 79, no. 1, pp. 22–30.

Watson, E. E., & Schneider, H. 1999. Using ERP systems in education, Communications of AIS, 1(2), Article 3.

Willcocks, L. P. & Sykes, R. 2000. The Role of the CIO and IT Function in ERP, Communications of the ACM, vol. 43, no. 4, pp. 33-38.

Copyright for articles published in this journal is retained by the authors, with first publication rights granted to the journal.

By virtue of their appearance in this open access journal, articles are free to use, with proper attribution, in educational and other non-commercial settings. Original article at: http://ijedict.dec.uwi.edu//viewarticle.php?id=658&layout=html

|